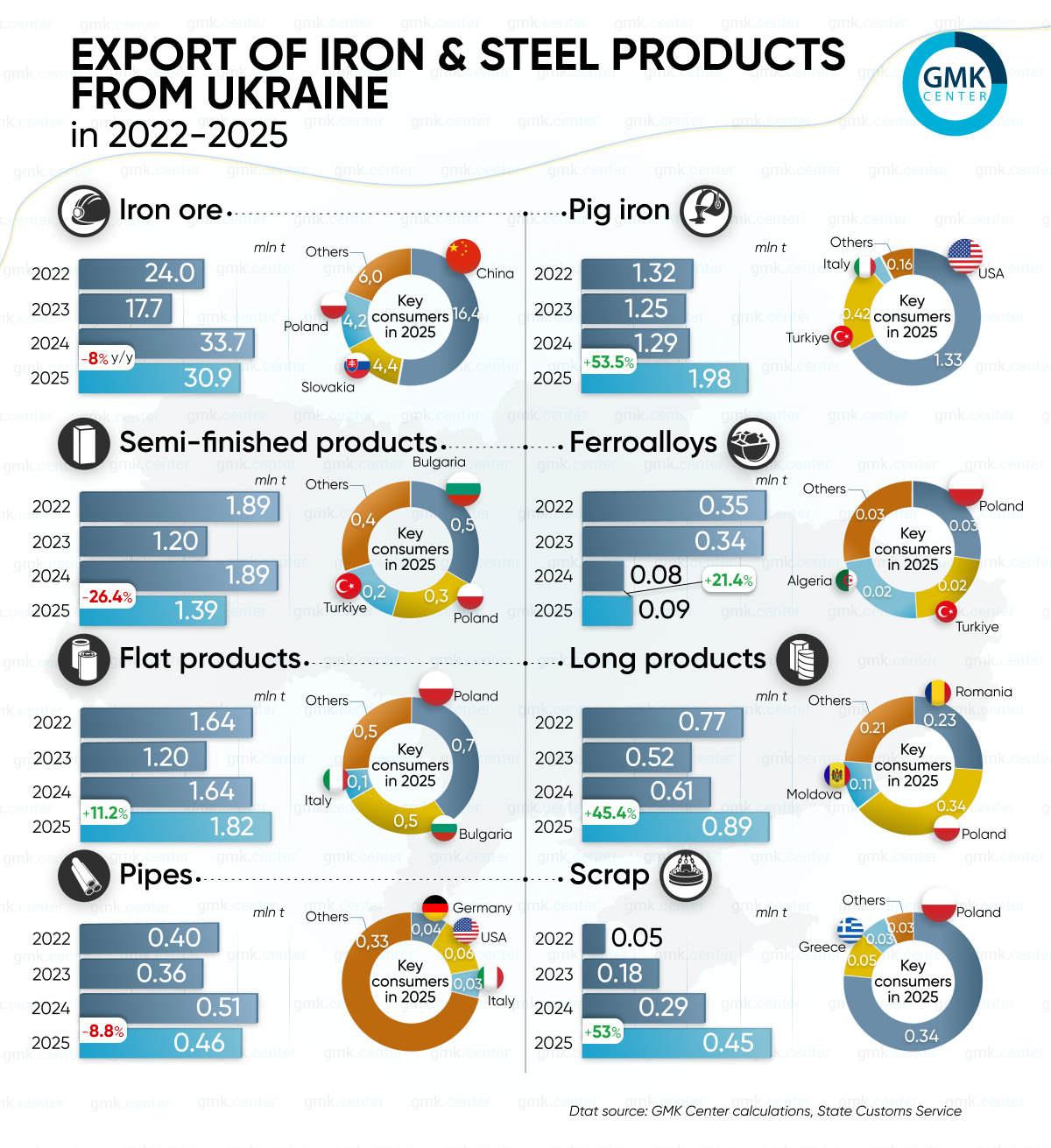

In 2025, Ukraine’s iron and steel industry continued to increase its presence in the global market. Product export volumes increased in most segments, with a decline recorded only in shipments of iron ore, semi-finished products and pipes.

Thus, exports of raw materials decreased by 8% last year compared to 2024, from 33.7 million tonnes to 30.99 million tonnes, respectively. The largest volumes of raw materials were sent to China – 16.41 million tonnes, which is 8.7% more year-on-year. At the same time, trade with European countries declined, which affected the overall indicator. Exports to Slovakia decreased by 11.4% y-o-y, to 4.4 million tonnes, and to Poland – by 18.1% y-o-y, to 4.17 million tonnes.

Shipments of semi-finished products abroad decreased by 26.4% y-o-y to 1.39 million tonnes, down from 1.89 million tonnes in 2024. Key consumers include Bulgaria, 461 thousand tonnes (-22.5% y-o-y), Poland, 291 thousand tonnes (+126.9% y-o-y), and Turkey, 216 thousand tonnes (+0.3% y-o-y).

Cast iron exports grew significantly during the year, by 53.5% y-o-y, to 1.98 million tonnes. The bulk of the product was exported to the United States (1.33 million tonnes, up 41.6% year-on-year), Italy (416,000 tonnes, up 346% year-on-year) and Turkey (75,000 tonnes, down 26.4% year-on-year).

Ferroalloy exports grew by 21.4% y-o-y to 94 thousand tonnes, mainly to Poland – 26 thousand tonnes (+24% y-o-y), Turkey – 20 thousand tonnes (+33.5% y-o-y), and Algeria – 21 thousand tonnes (0 thousand tonnes in 2024). At the same time, shipments of ferrous metal scrap increased to 449 thousand tonnes (+53% y/y). Poland is the key export destination – 344 thousand tonnes (+38.2% y/y). Another 48 thousand tonnes (+41.7% y/y) were sent to Greece, and 27 thousand tonnes to Italy (0 thousand tonnes in 2024).

Flat steel exports in 2025 increased by 11.2% compared to 2024, to 1.82 million tonnes, while long steel exports increased by 45.4% y/y, to 892,000 tonnes. In the flat steel segment, the largest consumers are Poland – 744 thousand tonnes (+19.3% y-o-y), Bulgaria – 461 thousand tonnes (+17.7% y-o-y), and Italy – 136 thousand tonnes (-10.3% y-o-y), while in the long products segment, the largest consumers are Romania – 233 thousand tonnes (+93.6% y-o-y), Poland – 336 thousand tonnes (+57.3% y-o-y), and Moldova – 108 thousand tonnes (+31.8% y-o-y).

Last year, pipe shipments abroad dropped by 8.8% year-on-year, to 465,000 tonnes. The United States received 60,000 tonnes (-35.2% y-o-y), Germany – 40,000 tonnes (-20.3% y-o-y), and Italy – 31,000 tonnes (-16.4% y-o-y).

The results for 2025 show a mixed export picture for the Ukrainian iron and steel complex. The decline in shipments of iron ore and semi-finished products reflects the structural weakness of the European steel market, where demand remains depressed due to industrial stagnation and high production costs. The reorientation of part of the ore flows to Asia was not able to fully compensate for the reduction in exports to EU countries.

On the other hand, the growth in exports of pig iron, scrap and finished rolled products indicates that Ukrainian companies are adapting to changes in demand and exploiting niche opportunities in foreign markets. Increased supplies to the US and countries in Central and South-Eastern Europe supported overall export volumes, despite limited production and logistics capabilities.

Further export dynamics in 2026 will largely depend on the recovery of steel consumption in the EU, the trade policies of key importers, and the ability of the Ukrainian iron and steel complex to remain competitive in wartime and amid intensifying global competition.

Source: https://gmk.center