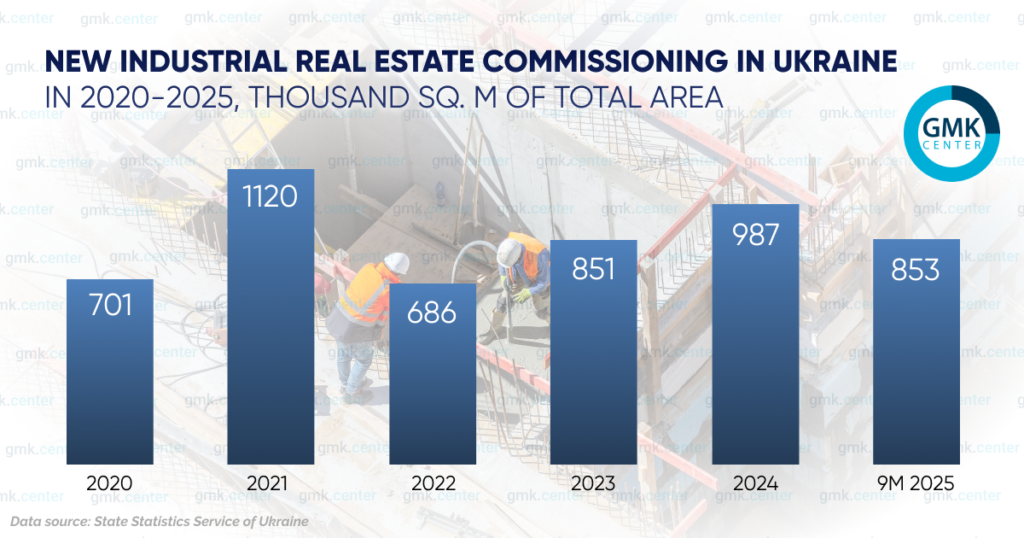

Following the onset of full-scale aggression, the commissioning of industrial space predictably declined sharply but subsequently began to recover. As of January–September 2025, the commissioning of industrial space increased by 23% year-on-year—to 852,500 square meters. It should be noted that by the end of 2024, this figure had increased by 16% year-on-year—to 987,000 square meters. This is only 12% less than in pre-war 2021.

Industrial construction has become the core of the industry, overtaking infrastructure. By the end of 2025, non-residential construction, which grew by 27.4% year-on-year, became the driver of the entire construction sector, overtaking the civil engineering segment (3.6% year-on-year). At the same time, industrial construction became the driver of the entire non-residential segment. The share of industrial real estate commissioning in the total volume of non-residential real estate commissioning increased significantly—to 37% in 2024–2025 from 20–22% in the pre-war years of 2020–2021.

This indicates that investors are increasingly favoring investments in Ukraine’s manufacturing sector. It is important to note that the projects for 2024–2025 involve new construction, rather than the relocation of existing facilities, which was the driver of demand for industrial real estate in 2022–2023.

Among the major industrial facilities commissioned in 2025, the Avesterra Group’s chicken processing plant in the Volyn region with €60 million in investments, the Nestlé pasta production plant in Volyn worth €42 million, and the Bakery Food Investment frozen bakery products facility opened in the Zakarpattia region for 400 million UAH.

The general characteristics of all production projects (sample size: 81 projects) launched in 2022–2025 are as follows:

Another distinctive feature of the Ukrainian industrial construction market is the lack of transparency. The locations of newly established enterprises fulfilling military contracts are often not disclosed, even in detail.

Regional trends

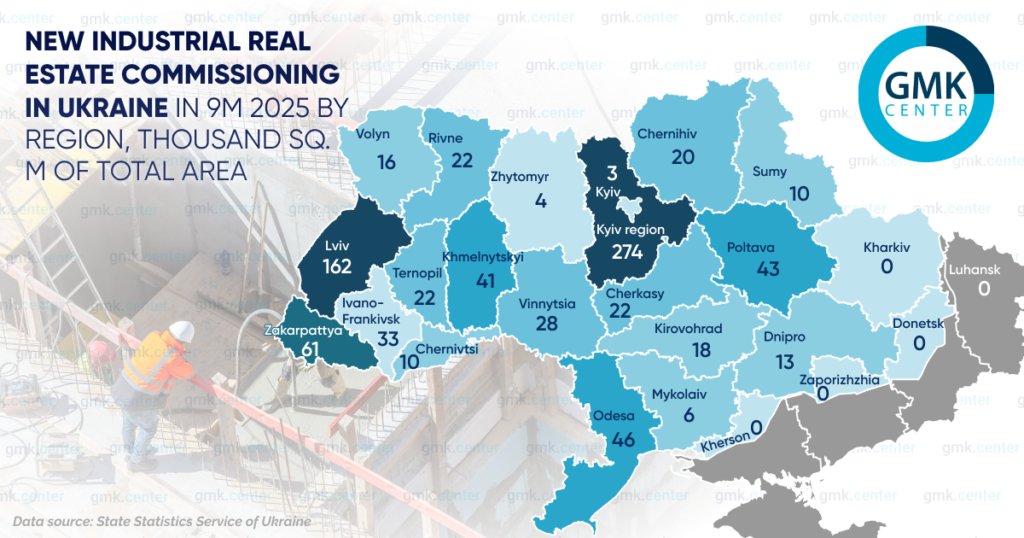

The trend toward the construction of new industrial real estate in the western and central regions of Ukraine emerged even before the war. Full-scale aggression has only intensified this trend. Among the leaders in the commissioning of industrial facilities based on the results of the first nine months of last year were Kyiv (32.3%), Lviv (19%), Zakarpattia (7.1%), Odesa (5.4%), and Poltava (5.1%) regions.

These figures clearly show that Ukraine’s western regions—which are relatively safe amid the war—are becoming hubs for industrial construction and industrial development. New logistics hubs and manufacturing centers, geared specifically toward exports, are emerging in the western regions.

Previously, the industrial regions of Kharkiv and Zaporizhzhia were among the leaders, but due to war-related risks, they are now reporting zero new industrial facility completions. The Dnipropetrovsk region has significantly lost ground: based on January–September figures from last year, its share fell to 1.5% from 8% in 2021. At the same time, the Odesa region, despite constant shelling, remains an attractive region: its share of new industrial real estate commissioning for the first nine months of last year stood at 5.4%.

Ambitious plans

The total floor area of industrial buildings and warehouses in the pre-construction phase in January–September 2025 decreased by 29% year-on-year, to 1.18 million square meters. At the same time, by the end of 2024, this figure had nearly doubled—to 2.3 million square meters from 1.2 million square meters in 2023. As early as 2024, the volume of planned industrial construction was 35% higher compared to 2021 levels. In other words, current plans for industrial real estate construction exceed pre-war levels.

Among the publicly announced industrial projects, the following are worth noting:

A significant portion of new production facilities and warehouses are being built or opened in industrial parks. Some companies locate their production there due to tax and customs incentives, while others do so because of the availability of engineering and other infrastructure. Additionally, new production facilities and warehouses are already being constructed with certain elements of backup power supply.

The western regions—Lviv (20) and Zakarpattia (12), as well as Kyiv (15)—led in the number of registered parks as of the end of last year.

The trend in the construction of new production facilities in industrial parks is positive. By the end of last year, 37 plants were under construction or had already been completed, whereas by the end of 2024, this figure stood at 25 enterprises.

Thus, the Ukrainian industrial construction market is demonstrating strong recovery momentum despite the ongoing full-scale war. The annual growth in the commissioning of industrial space, the exceeding of pre-war figures in terms of planned construction volume, and the active development of industrial parks point to significant prospects for the Ukrainian industrial sector.

Source: https://gmk.center