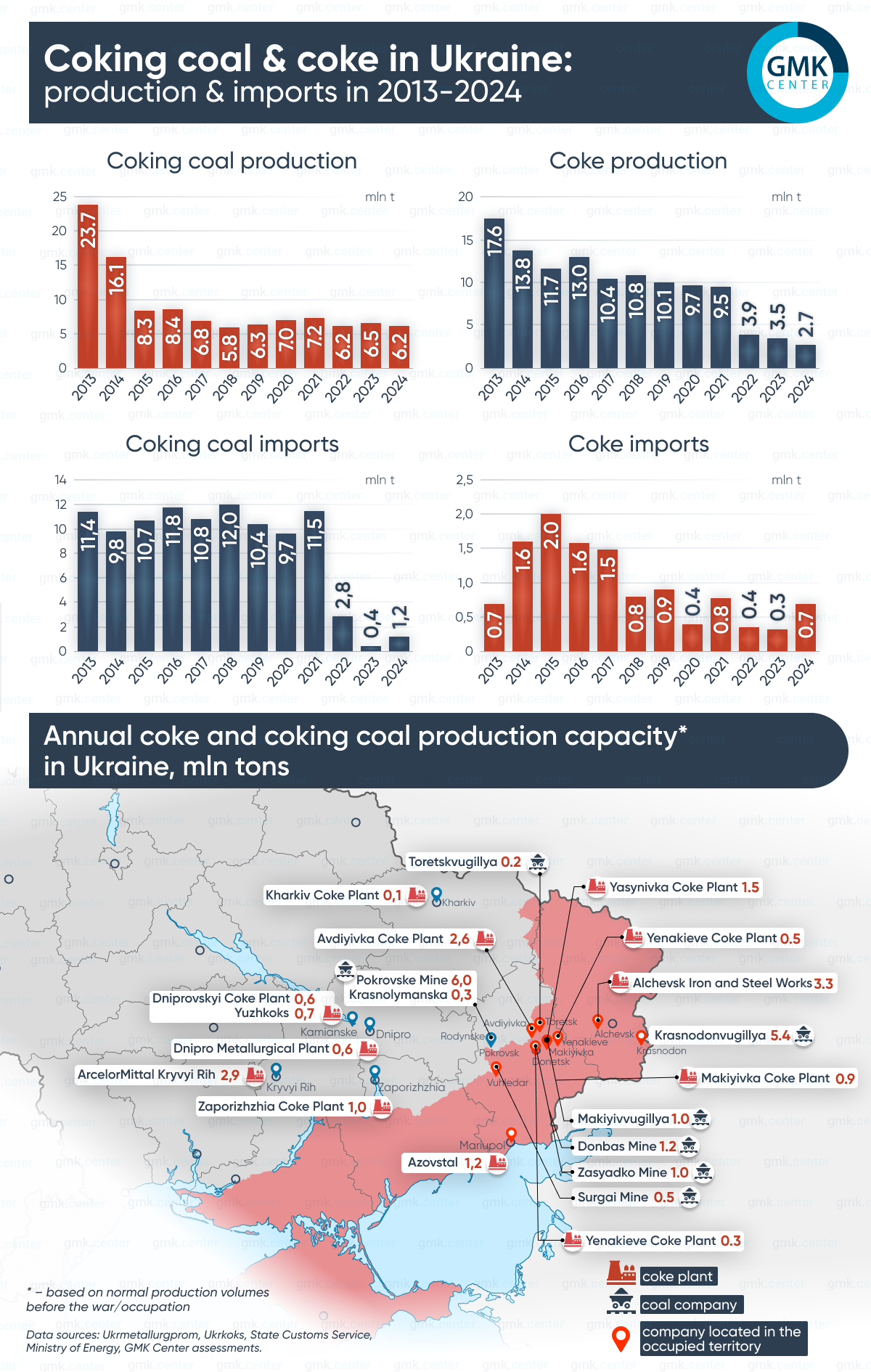

There were 7 enterprises manufacturing coke for pig iron production in the occupied territories

Between 2013 and 2024, Ukraine’s coking coal production plummeted by 74%, while coke production dropped nearly 85%. Imports of coking coal decreased by 89% during this period, driven by a decline in steel production, although coke imports have returned to 2013 levels.

Before the war, Ukraine was one of only four countries globally that was self-sufficient in raw materials for steel production, including coal, coke, iron ore, manganese ore, and ferroalloys. In 2013, Ukrainian mines produced 23.7 million tons of coking coal. Mines such as Krasnodonvugillya, Zasyadko Mine, Makiyivvugillya, and Donbas Mine, located in the non -controlled areas of Donetsk and Luhansk regions, collectively produced 8.6 million tons of coking coal.

Additionally, five coke plants were situated in the occupied territories, including coke batteries that were part of the Alchevsk Iron and Steel Works. During 2022–2024, Russian military forces destroyed critical facilities, including Azovstal, which had a coke capacity of 1.2 million tons, and the Avdiyivka Coke Plant, once one of the largest in Europe. GMK Center estimates that Ukraine lost approximately 64% of its coke production capacity between 2014 and 2024.

Some of the facilities have been completely destroyed, and mines in occupied areas have been flooded, making it nearly impossible to resume production quickly, even if the territories are retaken. Compounding the challenges, the suspension of production at the Pokrovske Mine which share in the Ukrainian coking coal market in 2024 was 66% poses a significant risk to the industry.

Transitioning to imported raw materials, such as coke and coking coal, is expected to significantly strain the financial health of Ukrainian steel companies. This will impact their ability to sustain operations, invest, pay debt, and support social programs. As competitiveness declines, Ukrainian steel exporters may face mounting pressure to limit shipments to markets with high transportation costs, while iron and steel production volumes in Ukraine are likely to decline.

Source: https://gmk.center/