The steel industries of Ukraine and the European Union are facing serious challenges, but the nature of these challenges is very different. In the EU, the main agenda is green transformation. European steelmakers are under pressure to decarbonize, reduce emissions, and adjust to stricter climate regulations. In Ukraine, the priority is more basic and urgent: survival under the conditions of war.

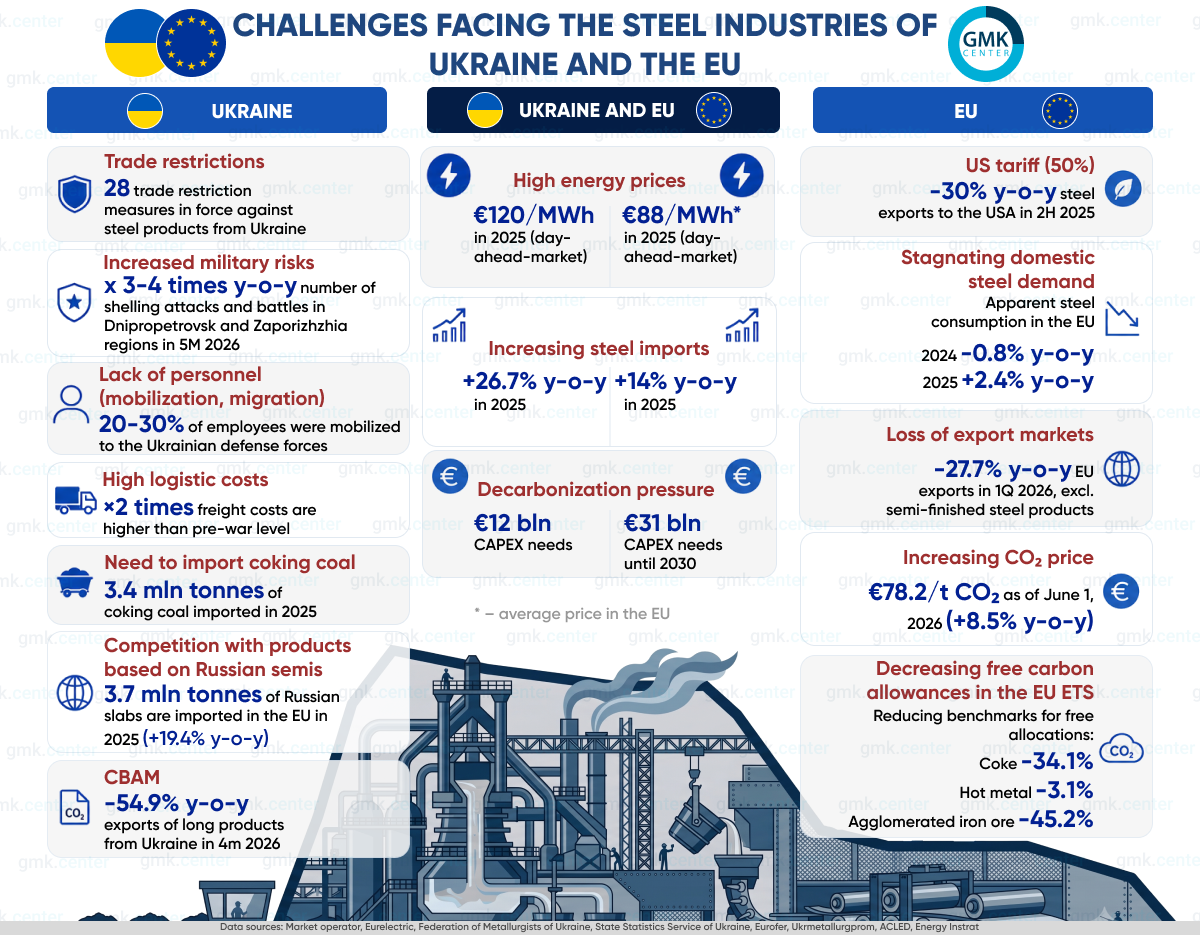

The Ukrainian steel industry operates under constant military risk. According to the data in the infographic, the number of shelling attacks and battles in Dnipropetrovsk and Zaporizhzhia regions increased three to four times year-on-year in the first five months of 2026. These regions are central to Ukraine’s steel production, so military pressure directly affects industrial stability and production output.

Ukrainian steelmakers also face a shortage of workers, as 20-30% of employees have been mobilized to the Ukrainian defense forces. Logistics remain another major burden, with freight costs at least twice as high as before the war. In addition, Ukraine had to import 3.4 million tonnes of coking coal in 2025, reflecting the disruption of domestic supply chains (loss of Pokrovske mine).

By contrast, the EU steel industry is mainly dealing with the costs of green transition decreasing competitiveness of European companies. EU producers face high electricity prices, with the average day-ahead market price reaching €88/MWh in 2025. They also face growing carbon costs: the CO₂ price reached €78.2/t as of June 1, 2026, up 8.5% year-on-year. Free allocation benchmarks under the EU ETS will be reduced leading to increased carbon costs of European steel producers. Decarbonization will require massive investment, with estimated capital expenditure needs of €31 bln by 2030.

However, Ukraine and the EU also share several problems. Both face high energy prices and growing import pressure. EU steel imports increased by 14.0% year-on-year in 2025, while Ukraine’s steel imports rose by 26.7%. Both industries are also affected by trade disruptions. For example, EU steel exports to the United States fell by 30% year-on-year in 2H 2025 after the introduction of 50% U.S. tariffs. Ukraine continues to face 28 trade restriction measures against its steel products.

These shared pressures create space for cooperation as the EU needs secure, reliable, and low-carbon steel supply chains which will support competitiveness of European steelmakers. Ukraine needs market access, investment, and support for recovery. Cooperation could focus on integrating Ukraine into European supply chains, supporting energy security, and preparing Ukrainian steelmakers for future decarbonization.

Source: https://gmk.center